Lump sum vs. monthly discipline — which builds wealth faster?

Will Koenig • March 26, 2026

Selling a home is an opportunity for wealth-building

1. Manage a monthly budget, keep spending in check, and invest consistently for 30 years

2. Invest a $400K lump sum from the sale of an appreciated asset once

I respect advisors who spend years cultivating relationships with business owners waiting for the liquidity event.

Meanwhile, every one of their clients owns a home.

And most will sell multiple times during your working relationship.

Think of each home sale as a mini-liquidation opportunity.

(that often are missed during the excitement of a move)

Here's what gets missed:

A simple debt consolidation can free up cash flow. But it only works if spending habits stay in check.

A home sale can create a tax-free lump sum that doesn't require monthly discipline. It just compounds.

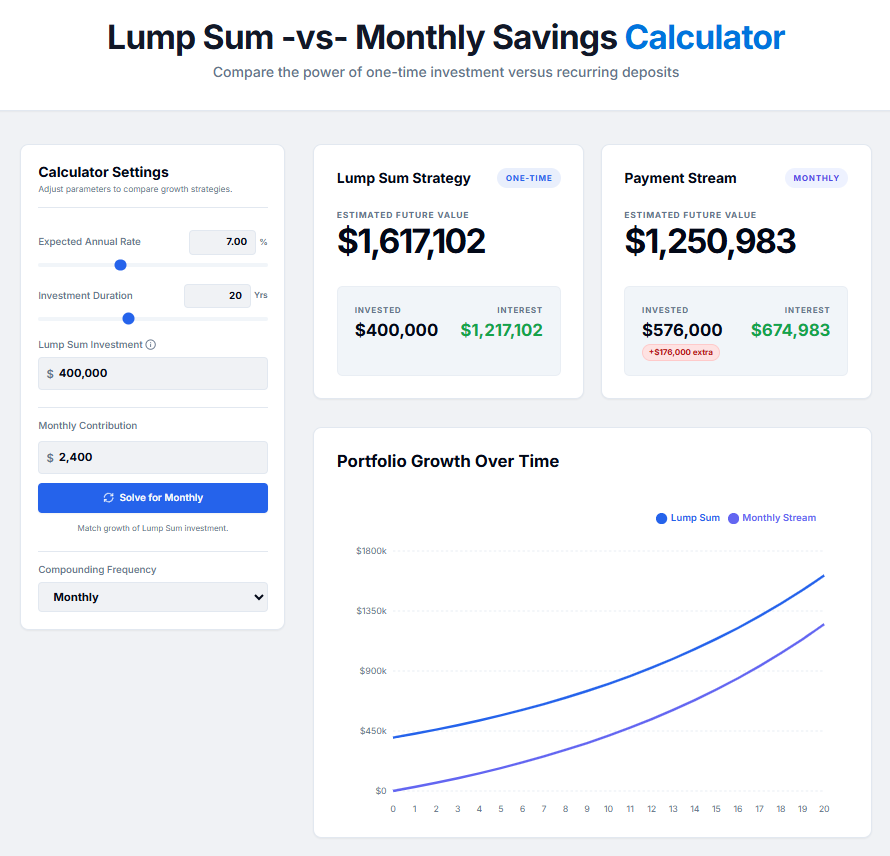

Look at the math: $400K invested once at 7% over 20 years = $1.62M.

The equivalent monthly contribution to reach the same result? $2,400/month for 20 years.

That's $576K that was earned but not spent.

The lump sum wins by over $300K in invested capital and requires zero behavioral change.

Why this matters:

People revisit their financial plan during life milestones.

Those milestones coincide with home changes—upsizing, downsizing, relocating, divorce, inheritance.

If we coordinate their home strategy with their wealth strategy during these transitions (what I call a Purchase Pivot),

we can create tax-free lump sums that advance the plan without feeling like a sacrifice.

Part of this is emotional: found money doesn't hurt like earned money.

Part of this is behavioral: life milestones trigger planning adjustments.

Part of this is math: lump sums compound faster than monthly contributions.

If your clients are considering a move in the next 12 months, let's talk about aligning their home plan with their wealth plan.

Sometimes the fastest path to more investable capital isn't tighter budgeting.

It's better liability structure and strategic timing around real estate.

Yours to count on,

-Will

Federal student loan repayment changes beginning July 1 could affect your mortgage debt-to-income ratio. Learn how RAP, IBR, and standard plans may impact homebuying power.

For decades, most mortgage lending has relied on Classic FICO.

Classic FICO gives lenders a snapshot of your credit at one point in time. It looks at things like payment history, balances, length of credit, credit mix, and recent credit activity.

Many homeowners feel stuck.

On one hand, you may have a mortgage rate that’s far lower than today’s market rates. Giving that up can feel like a mistake.

Homeownership is not just about getting the keys.

It is about caring for the place you live, protecting the investment you made, and making smart financial decisions along the way. At NEO Home Loans, we believe successful homeownership is built one month at a time through education, planning, and proactive support.

Do we make an offer and hope everything works out?

Do we wait and risk losing the home?

Do we rush our current home onto the market?

Unfortunately, this is where many homeowners find themselves.

Nobody wants to feel like they bought at the “wrong time.” Especially after watching headlines bounce between “housing crash,” “record prices,” and “rates are too high.”

If you’re thinking about moving, you’ve probably run into this problem:

You want to buy your next home…

But you feel like you have to sell your current one first.

When most people look at a mortgage payment, they only see what it costs today.

But that may not be the best question.

A better question could be:

What will this same payment feel like 10 years from now?

The housing market is changing… and most buyers haven’t caught up yet.

For the past few years, sellers had all the control. Homes sold fast. Buyers competed aggressively. And negotiating power was almost nonexistent.

That’s no longer the case.

Today, we’re seeing a clear shift toward a more balanced market, and that creates opportunity if you know how to use it.

If you’re planning to buy a home this season, you’re stepping into a market full of opportunity.

More homes are coming to market. Activity is picking up. And it finally feels like you might have a real shot at finding the right home.

But there’s a challenge most buyers don’t realize until it’s too late.